What is plain language? (Part Four: Putting it all together in a process)

The first three parts of my series on defining plain language focused on the three aspects of the rhetorical triangle: (1) textual elements like style and organization, (2) reader outcomes like comprehension and usability, and (3) writer outcomes like organizational costs and benefits. To overcome the limitations of any one of those aspects when considered alone, several experts talk about plain language as the process by which successful workplace documents are created — a process in which all three aspects are integrated. That’s my focus here in Part Four.

The first three parts of my series on defining plain language focused on the three aspects of the rhetorical triangle: (1) textual elements like style and organization, (2) reader outcomes like comprehension and usability, and (3) writer outcomes like organizational costs and benefits. To overcome the limitations of any one of those aspects when considered alone, several experts talk about plain language as the process by which successful workplace documents are created — a process in which all three aspects are integrated. That’s my focus here in Part Four.

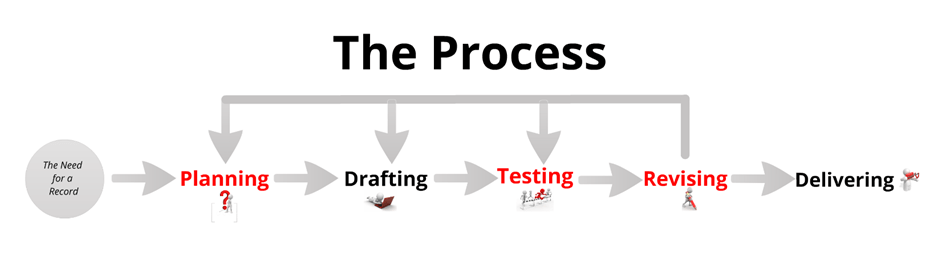

Minimally, creating a document requires drafting: putting words on paper (literally or figuratively). Sadly, amateurs operate as if this single step or activity = writing. To enhance the quality of documents and move amateurs toward expert status, writing teachers regularly add two additional steps to the process: intentional planning before you draft and revising after you have drafted. The wisest of these folks also promote some form of document testing in order to determine what and how to revise.

Let’s talk about the phases of the process shown in red using examples from the proposed mortgage loan estimate document created for the US Consumer Financial Protection Bureau (CFPB) project called Know Before You Owe by Kleimann Communication Group. I mentioned their exemplary work in an earlier post.

Planning

Pro workplace writers work their way through heuristic questions about the rhetorical context, message content, and content organization before they draft a document. Last year, I wrote a series of posts about a letter soliciting sponsorships for an outdoor sign at The First Tee of Tuscaloosa:

- Pros don’t settle for platitudes about audience described the principled way in which we analyzed our audience.

- Pros plan message content strategically described how we developed the content for the first draft.

- Pros plan message organization strategically described how we planned to organize the content for the first draft.

I don’t want to repeat what I wrote in those pieces. So let me just highlight some examples of the planning process for the loan estimate document.

In general, written messages are preferred for complex content and for situations in which a record of message delivery is needed. In the case of the loan estimate, both conditions were met. The Dodd-Frank Act required lenders to disclose information about mortgage loans to their customers after they apply for a mortgage and shortly before they complete the process. It also required combining the information from two separate forms.

Given the widespread interest in banking and financial practices, the CFPB judged that the high cost of creating a quality loan estimate document was worth it. One way they corroborated this interest was by holding a symposium with consumers and industry representatives in December of 2010.

The writers of the loan estimate knew their readers were the heterogeneous group of US consumers. They also knew some general things about that group of readers: (a) their ability to understand message content was low because the level of quantitative and financial literacy is low for around 50% of US adults and (b) their willingness to attend to and use the message content to make decisions was low because that is a characteristic of all US consumers. The team of writers had to develop both informative content (like examples and definitions) to address the audience’s inability to understand mortgage loan details and persuasive content (like evidence) to address the audience’s unwillingness to pay attention to and use those details.

Before they began drafting, they read relevant documents and research, talked to CFPB staff and consumers, and brainstormed. After they began testing drafts, the writers also met with small business owners about using the new loan estimate.

Testing

Testing a draft document is the phase of the workplace writing process that most distinguishes you as a pro. I haven’t written much about the types of document testing. My goal is not to be exhaustive here. Instead, let me share how the writers of the loan estimate tested their document.

First, they posted drafts of the documents on the Know Before You Owe website and collected 27,000 comments.

Second, they used parallel design tests by creating two significantly different designs for the loan estimate. They implemented those two designs in eight document versions based on four different loan details. In Round 1, they presented these document versions to seven English-speaking consumer participants, two Spanish-speaking consumer participants, and two mortgage lender participants in Baltimore. Using one-on-one interviews, they asked participants to read-and-think aloud and to answer comprehension questions; they also asked lenders to answer implementation questions.

Even when the benefit of a quality document doesn’t warrant the expensive testing done for the loan estimate, testing is still possible — and warranted. Editorial or expert review is certainly less costly. But even reader testing can be done on a shoestring budget. To learn more about testing documents, you can begin with the guidelines on usability testing from the federal government’s plain language site.

Revising

For the loan estimate, testing suggested numerous revisions to the textual elements in both designs. Among the most serious issues identified from Round 1 testing, the writers learned (a) consumer participants needed more clarity around the monthly loan payment and the total monthly payment; and (b) they needed to address how the design could encourage consumers to read the Cautions at the same time as they read the Loan Terms. So writers revised a number of textual elements in both designs. A few specifics for Design 1:

-

To make the loan amount more prominent, they added the heading Loan Amount.

-

To simplify cognitive processing and keep all cautions together, they combined the content of Key Loan Terms and Cautions.

-

To draw attention to cautions, they added more emphasis to this word in headings with shading and all caps.

Testing & Revising (Again)

The writers used an iterative design process. That means they tested the revised versions of the loan estimate in Round 2 in Los Angeles. And then revised the content, organization, and style some more. And tested again in Round 3 in Chicago. And revised more. In all, there were ten rounds of testing in cities across the US followed by revisions.

So . . . What is plain language?

After four rather lengthy posts, here — with a drumroll — is how I understand the concept of a plain language document.

- It can be described as a set of text elements, including content (e.g., examples), organization (e.g., headings), style (e.g., verb voice), and mechanics (e.g., punctuation).

- The outcome of delivering the document is that it achieves the writer’s purpose, while minimizing costs and maximizing benefits for the writer’s organization.

- Other outcomes of delivering the document are target reader interest, comprehension, and ability to use the writer’s message.

- The only way to produce a plain language document (one that achieves #2 and #3) is to use a process for choosing text elements that incorporates planning, testing, and revising.

And, finally, describing plain language with fewer than all four of the items above is like describing only a portion of the elephant.

Beware of those who claim plain language is simpler than this. That would include those who make promises based on software tools or platitudes. And pay attention to those who include all four items. (See, for instance, the plain language checklist from the Center for Plain Language.)

No wonder becoming a pro who can produce plain language takes so much time and effort! But that’s what makes a pro so valuable.

Related articles

- What is plain language? (Part One: Elements of the text) (proswrite.com)

- What is plain language? (Part Two: Audience outcomes) (proswrite.com)

- What is plain language? (Part Three: Writer outcomes) (proswrite.com)